In 2025, the entire resource ecosystem increasingly focused on waste, recognising its crucial role in the circular economy.

Throughout the year, regulators around the world officially launched or tightened extended producer responsibility (EPR) schemes, fundamentally changing the economics of packaging.

The paradigm shift prompted the world’s brands, retailers and packaging producers to interrogate their products’ end-of-life journey in more detail than ever – often discovering that they didn’t have the data needed to make measurable circular improvements.

The media didn’t miss the significance of this pivotal year. As the packaging landscape shifted, our AI waste analytics system, Greyparrot Analyzer, was named one of TIME Magazine’s Best Inventions, and Fast Company called waste intelligence a “world-changing idea”.

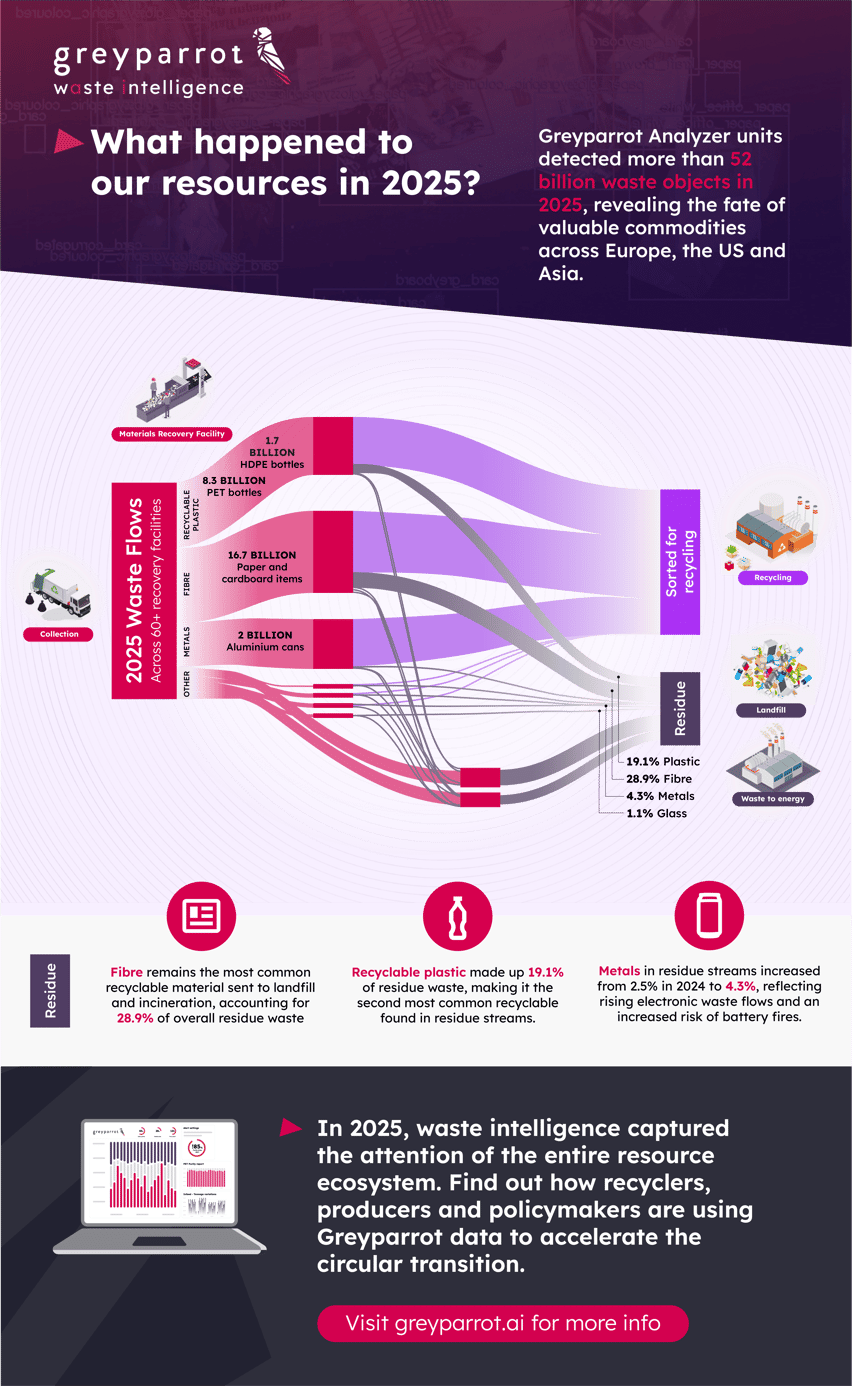

We’ve been preparing for this paradigm shift. This year, our global network of Analyzer units made more than 477 billion bounding box detections and analysed 52 billion unique waste objects – generating the data needed to answer the world’s new questions about waste.

The data for this year’s trend report came directly from facilities across more than 20 countries in North America, Europe and Asia, where recycling plant managers are using waste intelligence to manage leaner, more profitable facilities.

Here’s what this year’s global waste data tells us about recycling, materials and regulation:

Recovery rates remain high for key materials

As our Analyzer fleet expanded, we analysed over 1.24 million tonnes of recyclable material across 65 global recovery facilities this year. Just 103,000 tonnes were lost on residue lines, showing that the vast majority of recyclables were correctly sorted.

Preventing this material from being landfilled or incinerated avoids hundreds of thousands of tonnes of CO₂ emissions, reinforcing recycling’s critical role in circularity and emissions reduction.

Plastic recyclers are adapting to modern waste streams

We detected around 8.3 billion PET bottles entering recycling facilities this year. That’s 2 billion more bottles than we detected last year thanks to our increased global coverage – which makes the following insight even more encouraging:

Despite higher volumes, less recyclable plastic ended up in residue lines. Average recoverable plastic per Analyzer on residue lines fell from 3,000 tonnes in 2024 to 2,500 tonnes in 2025, showing that sorting facilities are adapting to process the growing plastic volumes more efficiently than ever.

Regulation doesn’t reflect plastic sorting realities (yet)

With that said, not all plastics are created equal. Recyclers captured a huge number of PET and HDPE bottles this year, but performance fluctuated wildly in 2025 – even within those categories.

One facility recovered 95% of the clear PET containers it processed, but just 15% of some coloured PET containers. That will cause a regulatory imbalance next year: under the current UK EPR system for instance, both of those containers would be taxed the same amount.

Small material differences translate to major recovery gaps. To make a meaningful impact on circularity in 2026, EPR regulation will need to get more granular and reflect the realities of plastic recovery – not just the intent behind packaging designs.

Glass is still getting recovered, but metal could pose a growing challenge

Glass remains consistently recovered, with its share in residue holding at just over 1% in 2025.

Meanwhile, metal, including 2 billion aluminium cans analysed by Analyzer units, saw its share of residue streams rise from 2.5% to 4.3% in a single year, highlighting a growing challenge.

That could partly be down to the fact that e-waste is the world’s fastest-growing waste stream. With the number of battery fires reaching record-highs in 2025, it presents a serious argument for investment in waste electrical and electronic equipment (WEEE) waste collection, recycling and responsible management.

Fibre waste trended lower, but remains a cost lever for MRFs

Analyzers identified 16.7 billion fibre items, these include materials like paper, corrugated card and greyboard. Fibre remains the most common recyclable material on global residue lines, but that proportion actually fell by 3.5% this year – perhaps reflecting the growing presence of materials like metal and plastics.

Last year, we reported that fibre was an emissions and cost-saving opportunity for MRFs, and that’s more pressing than ever in the current economic environment:

Emissions trading schemes (ETS) are set to impact waste incinerators in the UK and Europe over the next few years, who will be incentivised to burn higher proportions of fibre. Sorting facilities that can certify the amount of fibre in the material they send to those incinerators may be able to negotiate lower gate fees with incinerators as ETS comes into greater focus.

With margins thinning thanks to low-cost plastic imports and rising operating costs, minor cost-saving levers like those could add up to protect profits.

System-wide change will capture even more value

Even with this year’s high recovery rates, the proportion of recyclable material on global residue lines rose from 49.4% to 53%.

MRFs are adapting to growing volumes of waste with the help of automation, but a huge number of valuable secondary resources are still lost to landfill and incineration each year. Reversing that trend will require action beyond the recovery facility.

In many cases, packaging material is technically recyclable, but isn’t designed with real-world sorting systems in mind. For example, Deepnest data revealed that seemingly small design changes like removing label sleeves can mean bottles are 3 times more likely to get recovered in sorting facilities.

With circular design now incentivised by policies like EPR and PPWR (Packaging and Packaging Waste Regulation), brands, retailers and packaging producers have a timely opportunity to make data-driven packaging improvements to reduce the chances of packaging ending up on residue lines.

In 2026 and beyond, waste intelligence must move from operational advantage at facility level to systemic transformation. When real-world waste data connects design, policy, infrastructure and markets, decisions stop being made in isolation - and the entire value chain begins to align around recovery.

This is how true circularity is built: not through isolated improvements, but through shared visibility into what is actually happening to material in the real world post-use.

Waste intelligence closes the data gap that has held the system back - and in doing so, will accelerate the circular economy for a more sustainable future.

Learn how we used Greyparrot Analyzer to gather the data for this report here.

.png?width=501&height=285&name=Events%20social%20card%20(5).png)

-1.png?width=501&height=285&name=webinar%20(1)-1.png)